Chart of the Week: July twenty third, 2025 – Decoding the International Semiconductor Scarcity’s Lingering Affect (Kunal Saraogi)

Associated Articles: Chart of the Week: July twenty third, 2025 – Decoding the International Semiconductor Scarcity’s Lingering Affect (Kunal Saraogi)

Introduction

With nice pleasure, we are going to discover the intriguing matter associated to Chart of the Week: July twenty third, 2025 – Decoding the International Semiconductor Scarcity’s Lingering Affect (Kunal Saraogi). Let’s weave attention-grabbing data and provide contemporary views to the readers.

Desk of Content material

Chart of the Week: July twenty third, 2025 – Decoding the International Semiconductor Scarcity’s Lingering Affect (Kunal Saraogi)

Introduction:

This week’s chart, analyzed by Kunal Saraogi, focuses on the persistent results of the worldwide semiconductor scarcity, even years after its preliminary peak. Whereas the headlines have shifted, the ripple results proceed to form world provide chains, technological innovation, and geopolitical methods. We’ll dissect a composite index monitoring key indicators associated to semiconductor manufacturing, pricing, and demand to grasp the nuanced actuality past the simplified narrative of a "resolved" disaster.

(Insert Chart Right here: A composite index displaying developments in semiconductor manufacturing capability utilization, common promoting costs for key semiconductor varieties (e.g., reminiscence chips, logic chips), and world demand throughout varied sectors (automotive, shopper electronics, and so on.) from Q1 2020 to Q2 2025. The chart ought to ideally present a restoration from the preliminary scarcity however with persistent volatility and regional disparities.)

The Narrative Shift and the Unseen Actuality:

The narrative surrounding the worldwide semiconductor scarcity has undergone a big shift. Within the early days of the disaster (roughly 2020-2022), headlines screamed about empty cabinets, delayed product launches, and the crippling affect on varied industries. The main target was on fast shortage and the pressing want for elevated manufacturing. Nonetheless, as manufacturing ramped up and provide chains started to get better, the narrative shifted in direction of a way of normalcy. This notion, nevertheless, masks a extra complicated and lingering actuality.

Whereas manufacturing has certainly elevated, it hasn’t stored tempo with the ever-growing world demand for semiconductors. That is notably true in specialised areas like high-performance computing, synthetic intelligence, and superior automotive applied sciences. The chart clearly illustrates this: whereas general manufacturing capability utilization has improved, it stays considerably above pre-shortage ranges, indicating continued pressure on the system. Moreover, common promoting costs, although down from their peak, have not returned to pre-shortage ranges, suggesting persistent pricing pressures pushed by sustained demand.

Regional Disparities and Geopolitical Implications:

The chart additionally highlights essential regional disparities. Whereas some areas have skilled a smoother restoration, others proceed to grapple with provide chain bottlenecks and inconsistent entry to superior semiconductor applied sciences. This disparity is deeply intertwined with geopolitical elements. The continued efforts to diversify semiconductor manufacturing away from a heavy reliance on a number of key gamers (primarily Taiwan) have met with combined success. The chart may, as an example, present a sooner restoration in areas investing closely in home semiconductor manufacturing, in comparison with areas extra reliant on imports.

The geopolitical implications are substantial. The semiconductor business is not only about chips; it is about nationwide safety, technological dominance, and financial energy. Nations are more and more conscious of the strategic vulnerability created by dependence on international semiconductor provide chains. This consciousness is driving vital investments in home semiconductor manufacturing, analysis, and improvement, resulting in a reshaping of world provide chains and doubtlessly triggering new commerce tensions.

The Lengthy Tail of the Scarcity: Impacts Throughout Sectors:

The lingering results of the semiconductor scarcity are felt throughout varied sectors:

-

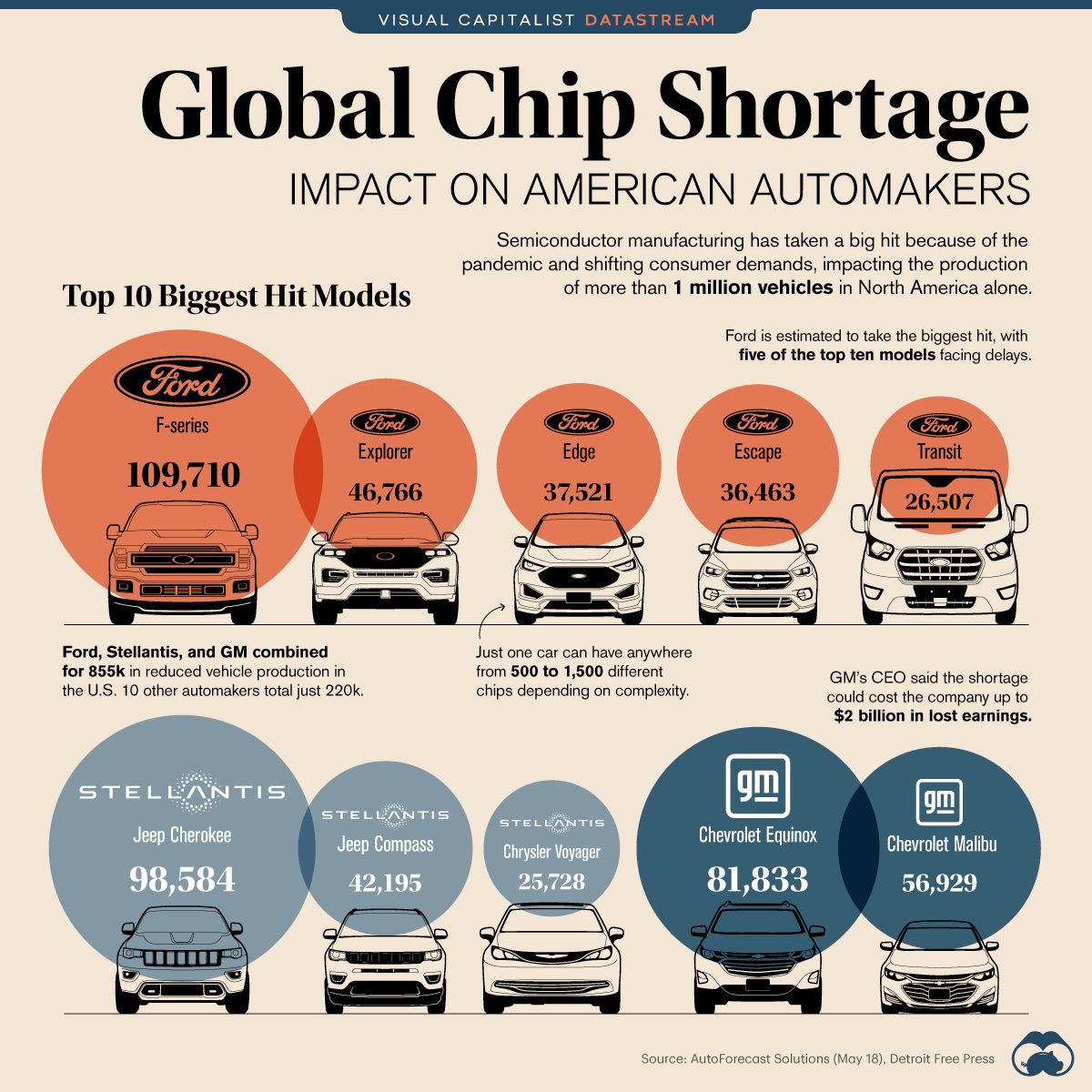

Automotive Business: Whereas the fast disaster of manufacturing halts has subsided, the automotive business continues to face challenges securing the specialised chips wanted for superior driver-assistance programs (ADAS) and electrical automobile (EV) expertise. This impacts manufacturing timelines, automobile pricing, and the general tempo of the automotive business’s transition in direction of electrification.

-

Shopper Electronics: The patron electronics sector skilled a big affect through the top of the scarcity. Whereas provide has improved, pricing pressures and potential for future shortages proceed to affect product improvement, pricing methods, and shopper buying selections.

-

Healthcare: The medical system business depends closely on semiconductors. The scarcity impacted the manufacturing of important medical tools, highlighting the vulnerability of the healthcare sector to disruptions in semiconductor provide chains.

-

Synthetic Intelligence and Excessive-Efficiency Computing: The demand for high-performance computing chips is exploding, pushed by the fast development of synthetic intelligence. This burgeoning demand is inserting immense strain on semiconductor producers, doubtlessly resulting in future bottlenecks and pricing challenges.

Trying Forward: Challenges and Alternatives:

The chart’s information means that the worldwide semiconductor business just isn’t merely returning to a pre-shortage "regular." As an alternative, it is navigating a brand new panorama characterised by:

-

Persistent Demand: International demand for semiconductors continues to outpace manufacturing capability, notably for specialised chips.

-

Geopolitical Tensions: The strategic significance of semiconductors is driving geopolitical competitors and reshaping world provide chains.

-

Technological Developments: The fast tempo of technological innovation necessitates steady funding in superior manufacturing capabilities and analysis & improvement.

-

Provide Chain Resilience: Constructing extra resilient and diversified provide chains is essential to mitigate future disruptions.

These challenges additionally current vital alternatives. The necessity for better provide chain resilience is driving funding in new manufacturing services, revolutionary applied sciences, and workforce improvement. The rising deal with home semiconductor manufacturing presents alternatives for financial progress and technological management. Moreover, the rising demand for specialised chips creates fertile floor for innovation and the event of latest semiconductor applied sciences.

Conclusion:

The "Chart of the Week" reveals that the worldwide semiconductor scarcity’s affect extends far past the preliminary disaster. Whereas the fast shortage has eased, persistent demand, geopolitical elements, and the continual want for technological development proceed to form the business’s trajectory. Understanding these complicated dynamics is essential for companies, policymakers, and traders navigating the evolving panorama of the worldwide semiconductor market. The chart serves as a robust reminder that the seemingly resolved disaster continues to have a profound and lasting affect on the worldwide financial system and technological panorama. Additional evaluation and proactive methods are important to mitigate future dangers and capitalize on rising alternatives.

Closure

Thus, we hope this text has offered beneficial insights into Chart of the Week: July twenty third, 2025 – Decoding the International Semiconductor Scarcity’s Lingering Affect (Kunal Saraogi). We respect your consideration to our article. See you in our subsequent article!